💰 What Is the Money Market?

The money market is where short-term, interest-bearing debt instruments are traded. In this market, financial institutions and other lenders provide funds to government and the corporate sector. The term is usually anything up to 12 months, but it can include terms of up to three years. Instruments in this market are usually seen as low risk, but returns are also lower. Instruments in this market is typically highly liquid.

Examples of instruments traded in this market include:

- Treasury bills – Short-term debt issued by the government to fund its deficit. The deficit is the shortfall when government expenditure exceeds its income (revenue).

- Call deposits – Money is deposited in an interest-bearing account and can be called back on demand. Normally, the larger the amount invested, the higher the interest rate.

- Negotiable Certificates of Deposit (NCDs) – These can be traded after issue, while a fixed deposit cannot be traded.

- Promissory notes – A written promise to pay a specific amount at a future date.

These instruments are issued by banks, corporates, and government entities, usually with maturities under a year. The goal? Liquidity, capital preservation, and modest interest income.

Minimum investment criteria and the need for investment expertise to invest in these instruments make it an unlikely place for individual participation.

🧭 How Individual Investors Can Access It Indirectly

You don’t need millions to benefit from money market dynamics. Here’s how retail investors typically gain exposure:

1. Money Market Unit Trusts / Funds

These are mutual funds that pool investor money to buy short-term debt instruments.

You can invest with low minimums (sometimes as little as R500).

Examples include:

- Allan Gray Money Market Fund

- Coronation Money Market Fund

- Nedgroup Investments

- Old Mutual Money Market Fund

2. Bank Money Market Accounts

Offered by major banks like Standard Bank, FNB, and ABSA.

These accounts mimic money market returns and offer daily liquidity.

Interest rates vary based on your balance and term.

3. Fixed-Term Deposits with Short Maturities

While technically not part of the money market, they offer similar benefits.

You lock in your money for 1–12 months with predictable returns.

🧠 Why Use Money Market Instruments?

These instruments are suitable for investors with a short investment horizon (maybe a year or two). Because of the lower investment returns, they are not optimal for long investment horizons.

They’re ideal for:

- Emergency funds

- Parking cash between investments

- Reducing portfolio volatility

- Preserving capital while earning modest interest

- Providing liquidity

- Generating an income stream from interest

- Diversifying your portfolio

- Achieving short-term financial goals

Money market instruments typically offer lower returns than bonds and shares. They also lack the growth potential of stocks and may not keep pace with inflation as effectively as other investments.

🧮 Step-by-Step: How to Compare Financial Options

✅ 1. Use a Comparison Checklist

Here is an example checklist

| Feature | Option A | Option B |

|---|---|---|

| Type of Account/Product | Savings | Money Market |

| Interest Rate Shown | 5% Nominal | 4.8% Effective |

| Compounding Frequency | Monthly | Quarterly |

| Minimum Deposit | R500 | R1,000 |

| Access to Funds | Anytime | Limited |

| Fees or Penalties | None | R10/month |

| Final Effective Rate | ? | 4.8% |

🧠 Tip: Always compare the effective rate, not the nominal rate (unless the compounding frequencies are the same).

📊 2. Nominal vs. Effective Rates

What is the difference between nominal rates and effective rates

- Nominal Rate: The rate they say you’ll earn.

- Effective Rate: The rate you actually earn after compounding.

💡 If interest is added more than once a year, the effective rate will be higher than the nominal rate.

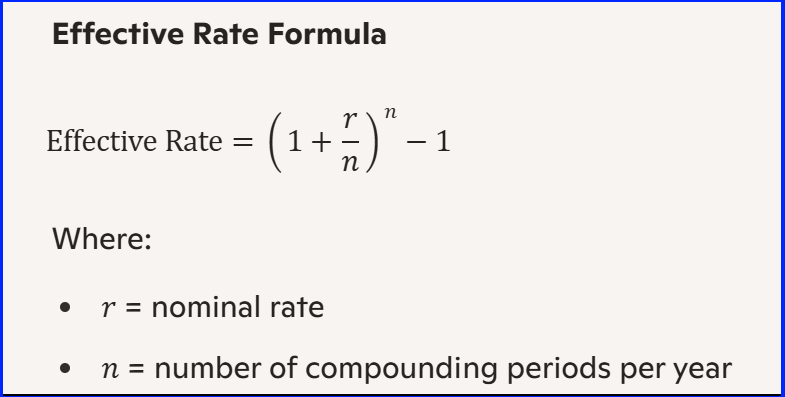

🧠 3. Formula to convert the nominal rate to an effective rate

You can use this formula

Or if you prefer Excel, you can use this formula:

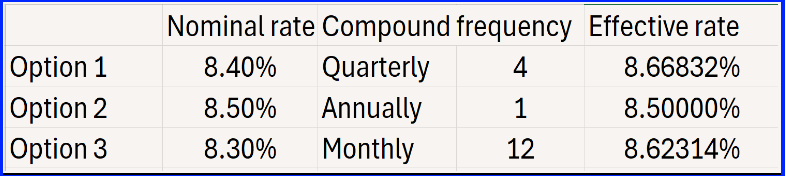

Example

Lets try this out. If the bank gives you these nominal interest rates and compound frequencies, which of these fixed deposits provides the highest return? Can you see why we can not simply compare the nominal rates if the compound frequencies differ. First convert it to the effective rate, then you know you are comparing apples with apples.

⚠️ Risks to Keep in Mind

Even though they’re low-risk, they’re not risk-free:

- Credit risk – Issuers could default

- Interest rate risk – Rising rates can affect returns

- Inflation risk – Returns may not keep pace with inflation

What about Tax?

Interest is taxable, and the after-tax return may be lower than inflation if the interest and inflation rate are very close. This means your capital could lose its buying power over time.

There is an income tax exemption available. At the time of writing, the first R23 800 for investors under the age of 65, and R34 500 for investors over the age of 65 is tax-free.

Here is a cool trick. If you know the interest rate you can calculate how much you can invest without paying income tax on the interest.

If you are younger than age 65, the interest exemption is R23 800. Let's say the investment you are looking at, pays 8% interest. You can calculate how much you must invest to take full advantage of the exemption and not pay tax.

Max amount to invest = Exemption / Interest rate.

The amount you can invest tax free is R 23 800 / 8% = R297 500

💼 Weekly Challenge: Compare Fixed Deposit Options

This week, your mission is to explore how banks offer different ways to grow your money.

🔍 What to Do:

- Visit your bank’s website (or any local bank you’re curious about).

- Look for fixed deposit options—these are savings accounts where you lock your money in for a set time and earn interest.

- Use the comparison checklist to compare at least two options. Even if you can’t find all the details, that’s okay! Just work with what you can gather. I just want you to explore and try to apply the information above.

✅ Your Checklist Might Include:

- Interest rate (nominal or effective)

There may be different interest rates depending on the amount invested - Minimum deposit required

- How long the money is locked in

- Access to funds (early withdrawal rules)

- Fees or penalties

- Compounding frequency (if available)

🧠 Your Goal:

Choose the option you think offers the best value based on the information you found. Be ready to explain your choice in simple terms. And remember to have fun!